By Judy Obae

- 25% Americans now use Buy Now Pay Later (BNPL) loans to afford groceries

- Nearly 1 in 8 U.S. households reported food insecurity in 2024, as inflation and stagnant wages strain budgets

As inflation continues to rise while wages remain largely stagnant, American households are facing unprecedented pressure to meet even their most basic needs. A 2023 study shows that 12.5% people were unable to afford food. Once a convenient way to finance big-ticket purchases, Buy Now Pay Later (BNPL) services are increasingly being used to cover essential expenses like food. This shift in consumer behavior reveals a deeper economic distress that goes beyond temporary hardship. The problem isn’t just individual choices, it’s a sign of widening systemic gaps. And it’s happening fast.

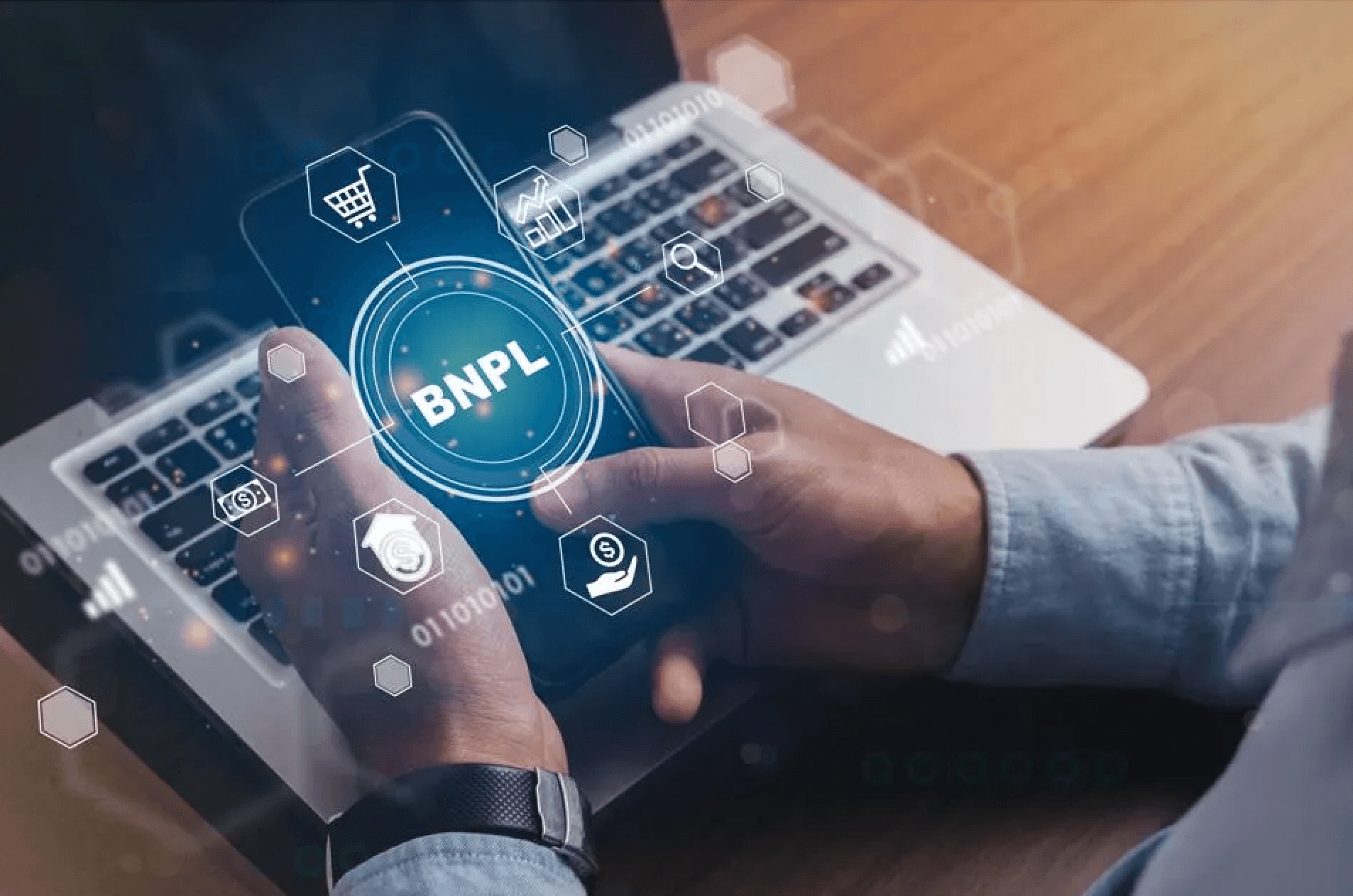

Why This Matters: The convergence of rising food costs and stalled wage growth has forced many Americans to reconsider how they pay for daily necessities. What’s even more alarming is that 76.8% of food-insecure households cited lack of affordability as the main reason for skipping meals. In this environment, BNPL services like Klarna, Afterpay, and Affirm are no longer just tools for spreading out the cost of a Peloton or designer shoes. They’ve become a lifeline. According to recent data, 25% of Americans now use BNPL to buy groceries, up from just 11% in 2022. This dramatic rise in dependency reflects a sobering reality: BNPL is not a financial convenience, it’s a symptom of survival.

The broader BNPL market reflects this transformation. Globally valued at $90.69 billion in 2020, it’s projected to balloon to $3.98 trillion by 2030. The biggest growth drivers? Young adults, digital adoption, and now, rising demand for flexible payments on essential goods. BNPL is expanding in healthcare and wellness too, as people finance everything from dental work to prescription medications. This repurposing of a financial tool built for consumer choice into one used for economic necessity raises serious red flags. BNPL may offer short-term relief, but with high late fees and no traditional credit checks, it can quickly turn into a cycle of debt especially for households already on the brink.

What Next: BNPL’s surge as a survival strategy signals a deeper failure in the economic safety net. Without policy interventions addressing wage stagnation and inflation, reliance on alternative credit tools will likely increase. Regulators, social service providers, and fintech firms must recognize this shift and act accordingly. Otherwise, BNPL may not just reflect economic desperation; it could deepen it.

CBX Vibe: ‘Hard Times‘ Baby Huey